Are you an expat who wishes to settle down in Spain? An investor who is eyeing the real estate here? Or are you one of the up and coming ambitious entrepreneurs who is considering the country an ideal place for launching their startup?

Then knowing how the Spain tax brackets work, what is residency status, and how you can ensure your compliance are some of the most important matters.

In this blog post, we cover it all. From tax residency and income brackets to corporate levies and exemptions, we discuss everything there is to know. And no, we don’t forget about that dreaded paperwork either!

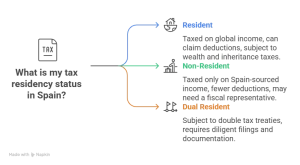

Understanding Tax Residency in Spain

Before you calculate a single euro in taxes, there is another thing you need to do first. You have to determine your tax residency status.

Spain distinguishes between its tax residents and non-residents. And that classification? It drives everything, including:

- What income gets taxed

- Which forms to file

- How much you pay

The tax office doesn’t just take your word for it either. They apply specific criteria to determine where your fiscal loyalty lies.

Who Qualifies as a Tax Resident?

So, what makes you qualify as a tax resident in Spain? You are one, if any of these following points apply to you:

- You spend more than 183 days in Spain during a calendar year. No, these days don’t have to be consecutive either. Your hotel receipts and credit cards can affirm the number of days of your stay in the country.

- Your primary professional or economic interests lie here. Precisely, your job, business, or investments are based in Spain.

- Your spouse and dependent minor children habitually live here.

Now, if any of the above apply, it means you are a tax resident. This status means you are going to be subject to taxation on your worldwide income, instead of your earnings within Spain.

Worried About Spanish Tax Compliance While Hiring or Relocating Staff?

Key Differences Between Non Resident vs. Resident

Your tax residency status imply significantly different things:

Residents

They are taxed on their global income. Residents also need to file their annual declarations and can claim deductions, allowances, and benefits. If you are a resident, you are also subject to wealth and inheritance taxes.

Non Residents

They are taxed only on Spain sourced income. It is generally subject to flat tax rates, with fewer deductions and obligations. If you are a non-resident, it’s highly likely you will be required to appoint a fiscal representative in Spain.

Dual Residency and Tie Breaker Rules

When someone qualifies as a tax resident in both Spain and another country, double tax treaties (dt as) apply. The oecd’s tie breaker criteria are used to resolve conflicts:

- Where you have a permanent home

- Location of personal and economic interests

- Where you habitually reside

- Your nationality

- Mutual agreement between the two countries’ tax authorities

These agreements help prevent double taxation. Although they require being diligent in filings and documentation.

Spain Income Tax System: An Overview

Spain operates on a progressive tax model, meaning the higher your income, the more tax you pay. personal income tax is split between national and regional components. Your effective tax rate will vary depending on which autonomous community you reside in.

Spain Income Tax Brackets 2025

Here are the national tax brackets for 2025:

- Up to €12,450: 19%

- €12,451 to €20,200: 24%

- €20,201 to €35,200: 30%

- €35,201 to €60,000: 37%

- €60,001 to €300,000: 45%

- Over €300,001: 47%

Regional tax rates are then layered on top. as a result, your total tax rate might be higher or lower depending on where you live.

Expanding Your Business Into Spain? Simplify Payroll and Tax Filing with Us

Regional Variations in Tax Rates

Spain’s 17 autonomous communities, including catalonia, andalusia, and madrid, have the power to set their own rates for the regional portion of income tax. for example:

- Madrid has among the lowest personal income tax rates in Spain.

- Catalonia applies one of the highest regional tax surcharges.

- Andalusia recently reduced regional taxes to attract more residents and businesses.

Understanding these differences is key to accurate tax planning, especially if you have flexibility about where to live.

| Region | Total Personal Income Tax Range (Approx.) | Notable Traits |

| Madrid | 19% – 43% | One of Spain’s most tax-friendly regions with lower regional surcharges. |

| Catalonia | 22% – 50% | Among the highest combined tax rates in Spain; higher surcharges for high earners. |

| Andalusia | 19% – 45% | Recently reduced tax rates to attract professionals and businesses. |

| Valencia | 20% – 48% | Moderate to high tax range; progressive structure similar to Catalonia. |

| Basque Country | 20% – 49% | Special tax regime; independent fiscal authority with unique adjustments. |

Are Taxes High in Spain Compared to Other Countries?

Spain’s income tax rates are in line with other developed european nations. While some expats feel the pinch due to a lack of familiarity with the system, Spain offers solid value in return. The tax revenue here supports:

- Public healthcare

- State pension systems

- Free or affordable education

- Reliable infrastructure and public transportation

Taxes can seem high comparatively with other countries, depending on your overall income and lifestyle. But once you factor in the benefits and the Average salary in Spain, the tax load seems to be every bit reasonable.

Other Personal Taxes in Spain

Spain levies several other personal taxes, some of which can catch expats by surprise. These include capital gains, wealth, and inheritance taxes.

Capital Gains Tax

Capital gains tax (cgt) applies when you sell property, stocks, or other assets. The rates are:

- Up to €6,000: 19%

- €6,001 to €50,000: 21%

- €50,001 to €200,000: 23%

- €200,001 to €300,000: 27%

- Over €300,000: 28%

If you reinvest gains in a new primary residence, you may be eligible for exemptions, especially if you are over 65.

Wealth Tax

Wealth tax applies if your net assets exceed €700,000, excluding your main home (up to €300,000 exempt). Rates are progressive, from 0.2% to 3.5%.

Some regions offer exemptions or apply reduced rates, but others (like catalonia) are stricter in enforcing the tax.

Inheritance and Gift Tax

Spain taxes both gifts and inheritance. And these rules vary wildly by region. There are various factors that influence how much tax you owe, including:

- Your relationship to the deceased or donor

- The value of the gift or inheritance

- The region where the assets are located

Close family members often receive generous deductions. But this isn’t something universal.

Taxation for Property Owners and Investors

Spain is a popular market for property investment, especially in tourist hotspots. But taxes related to property can be substantial, so it’s important to budget accordingly.

Vat and Transfer Tax on Property Sales

- New builds are subject to 10% Spanish vat rate

- Resale properties have a transfer tax of 6% to 10% imposed, depending on the region

Other costs such as stamp duty, legal fees, and notary services can add another 2% to 3%.

Local Property Taxes (ibi) and Capital Gains on Sales

Ibi is a local tax paid annually. It is based on the cadastral value of the property. Sellers also have to pay:

- Capital gains tax based on the appreciation since purchase

- Plusvalía Municipal, a local tax on land value increases

Rental Income Taxes for Residents and Non Residents

- Residents should declare their rental income as part of general income and can deduct costs like mortgage interest, repairs, and agency fees.

- Non residents are taxed at a flat 24% on gross income. If you are an eu or an eeu resident, that would be 19% for you. there are no deductions though, unless it has been covered under a treaty.

Corporate and Startup Taxes in Spain

Spain offers a relatively straightforward corporate tax structure. Plus, there are several incentives involved for small businesses and startups.

Corporate Tax Rates

- Standard rate is 25%

- The rate for startups is 15% for the first two profitable years

- For financial institutions and energy companies, the corporate tax rate is 30%

Special Incentives and Reliefs

- Beckham law is for attracting foreign professionals with a flat 24% tax on Spanish income

- Andalusia incentives offer tax breaks for companies relocating to southern Spain

- Sme deductions are available to small and medium enterprises

How to File Taxes in Spain

Filing taxes in Spain can be a challenge. Especially if you don’t speak Spanish or if you are not familiar with the system. Still, compliance is necessary. These are some major points that you should know:

Tax Deadlines and Forms

- Irpf declaration is the annual filing between april and june

- Form 100 is used for personal income tax

- Modelo 720 is mandatory declaration of overseas assets if they exceed €50,000

Late or incorrect filings can trigger steep penalties.

Filing Taxes in Spain for the First Time (Step-by-Step Guide)

If you’re filing taxes in Spain for the very first time, the process might seem overwhelming – but it’s quite manageable once you know what to do. Here’s a clear step-by-step guide to help you through it.

Step 1: Check Your Residency Status

Before you file, determine whether you’re a tax resident or non-resident. Your residency defines which income sources you must declare and which forms apply.

Step 2: Gather All Necessary Documents

Collect your:

- NIE (Número de Identificación de Extranjero)

- Proof of income (employment, rental, or investment)

- Expense receipts and deductible documentation

- Bank certificates or statements for interest/dividends

- Previous tax returns (if any)

Step 3: Register with Agencia Tributaria

If you haven’t already, register yourself with the Agencia Tributaria (Spanish Tax Agency). You’ll receive access credentials for Spain’s online tax system.

Website: https://sede.agenciatributaria.gob.es

Step 4: File Your Return Using Modelo 100

- Residents must use Modelo 100 to file their annual personal income tax (IRPF).

- The typical filing period runs from April to June each year.

- Make sure to include both Spanish and (if applicable) foreign income.

Step 5: Pay Taxes and Retain Proof

Once you’ve submitted your declaration, pay any outstanding tax directly through:

- The Agencia Tributaria portal,

- Authorized banks, or

- A registered gestor (tax agent).

Always save payment receipts and digital confirmation – they serve as proof of compliance.

How to Pay Taxes in Spain

Taxes can be paid via:

- Online using the agencia tributaria portal

- At authorized banks

- Through direct debit or with the help of a tax agent

Hiring a Tax Consultant or Gestor

Regional rules, language barriers, and complex forms have many expats relying on a tax advisor or gestor. If you work with an Employer of record in Spain, they might provide some form of tax support or referrals.

Double Taxation Agreements (DTAs)

Spain has dt as with over 90 countries to help individuals avoid double taxation and reduce tax burdens.

How DTAs Protect Expats

- The credit method offsets foreign tax paid against Spanish liability

- With exemption method, some income is excluded from Spanish taxation

- Treaties often define income types like pensions, dividends, and employment earnings

Most Common Countries with DTAs

Some of Spain’s most used dt as are with:

- United States

- United Kingdom

- France

- Germany

- India

Planning on Setting up a company in Spain? A DTA with your home country may impact your structure and tax strategy.

Exemptions, Deductions, and Allowances for Expats

The Spanish tax system provides various ways to reduce your tax burden if you know where to look.

Personal Allowances and Deductions

- Child allowances and dependent care deductions

- Spousal support or contributions to family units

- Mortgage interest on main residence

- Charitable donations

- Pension contributions

Capital Gains Exemptions for Over 65s

Seniors, of 65+ years age, who sell their main residence after living there for at least three years may be exempt from capital gains tax. this can significantly lower your overall tax exposure.

Beckham Law for Foreign Workers

Available to qualifying foreign professionals. Offers:

- Fixed 24% tax on Spanish income up to €600,000/year

- Exemption from taxation on foreign income

- Valid for six years

How to Reduce Your Tax Burden in Spain (Legally)

While Spain’s tax system may seem complex, there are several ways to minimize your liability without stepping outside compliance boundaries.

Contribute to Pension and Savings Plans

Voluntary pension contributions are deductible up to certain limits. By investing in an approved pension fund, you not only secure your retirement but also lower your taxable income.

Invest in Real Estate or Primary Residence

Homeowners may claim deductions on mortgage interest payments. Seniors who sell their main residence after living there for three years can often enjoy capital gains exemptions.

Claim Family and Dependent Deductions

Parents, caregivers, and spouses who financially support dependents can claim specific tax allowances. These are especially useful for expat families settling in Spain.

Donate to Approved Charities or NGOs

Charitable donations to certified organizations are tax-deductible, often up to 80% for the first €150 donated, and 35% thereafter.

Use Double Taxation Agreements (DTAs) Wisely

If you earn income abroad, check whether your home country has a DTA with Spain. These treaties allow you to offset foreign tax paid or exempt certain income, preventing double taxation.

Choose the Right Autonomous Community

As regional rates vary, choosing a tax-favorable region such as Madrid or Andalusia can help you reduce your overall liability if relocation flexibility exists.

Seek Professional Guidance

Tax laws in Spain change frequently. Working with a qualified tax consultant-or an Employer of Record (EOR) like Iberia EOR can ensure you claim all available deductions and stay compliant.

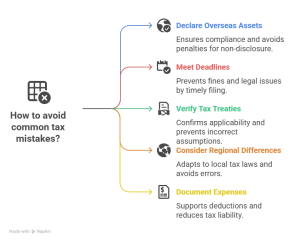

Common Tax Mistakes Expats Should Avoid

These are some mistakes you should watch out for:

- Not declaring your overseas accounts or property

- Missing deadlines, especially for modelo 720

- Assuming tax treaties apply automatically

- Ignoring regional tax differences

- Not keeping documentation of deductible expenses

Final Thoughts: Navigating the Spanish Tax Landscape

Taxes in Spain are layered and detailed, but with a bit of knowledge and preparation, they are manageable. Whether you are living in spain long term or investing from abroad, knowing your obligations helps you avoid fines and make the most of tax benefits.

Need help streamlining compliance, payroll, and filings? Iberia’s EOR services simplify the Back office burden so you can focus on what matters.

Want Stress-Free Employee Onboarding and Tax Management?

FAQs

How Do I Pay Taxes in Spain as An Expat?

You Can Pay Your Taxes via The Agencia Tributaria Website, through authorized banks, or using a local tax consultant.

Are Taxes High in Spain Compared to Other European Countries?

The taxes are usually in the mid to high range.

What Are the Spain Tax Brackets in 2025?

They range from 19% to 47%, plus regional surcharges.

Do I Have to Declare Income Earned Outside Spain?

Yes, if you are a tax resident. Global income must be declared, with possible relief via DTAs.